Opportunity remains but research is key – Secret Adverse

By: Doug Hall, Director, 3mc

Before looking at our recently launched “Secret Adverse” campaign…Let’s take a step back and understand the current specialist market and how it might play out throughout 2023.

As we see it, there are 2 main influencing factors that are, or will impact on the specialist mortgage market.

- The cost-of-living challenges – and what impact it will have on the profile of clients.

- The higher mortgage interest rate environment and why it has never been more important to quote clients accurately. 2 of the images below will demonstrate how inaccuracies might occur. As my father-in-law has said to me on many occasions, measure twice and cut once…

Going back to the cost of living first…We believe that we as an industry will see a greater percentage of clients with minor adverse, such as late payments on unsecured credit, smaller defaults and smaller CCJ’s. We also believe that the same client may well have a greater number of minor adverse entries on their credit files.

Moving onto the higher mortgage interest rate environment, it has never been more important to quote your perspective clients accurately, right at the front of the client mortgage journey.

Our “Secret Adverse” campaign has been designed to assist our mortgage advisers when looking at their specialist mortgage enquiries with a specific focus on minor adverse.

Click here for the Secret Lender Adverse guide (latest version)

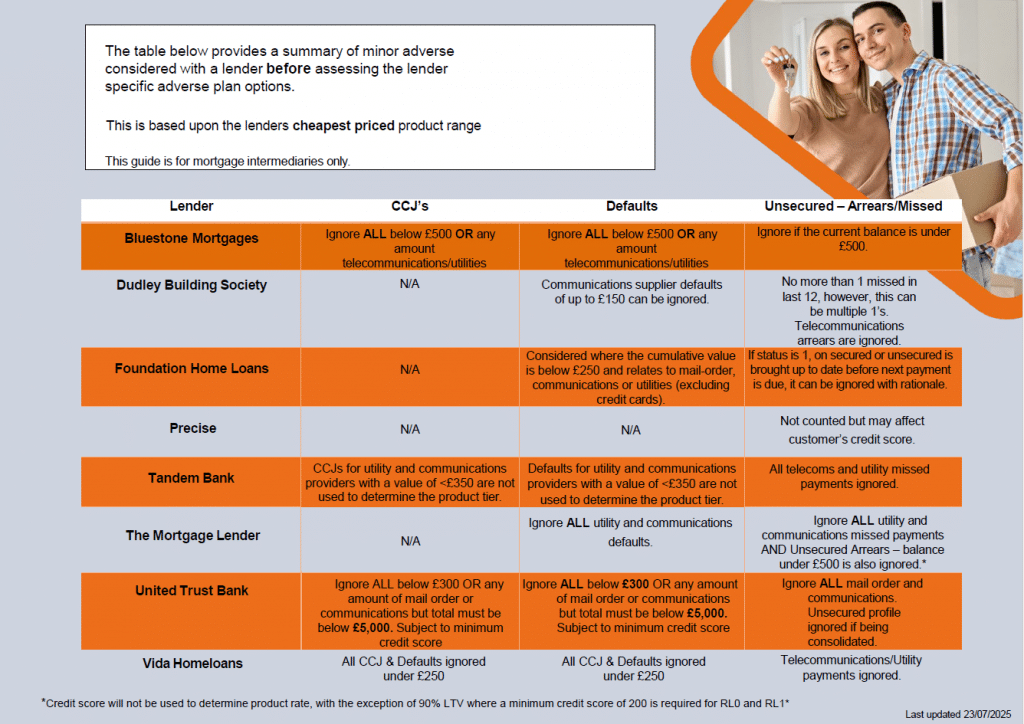

There are a number of specialist lenders who ignore certain categories of adverse when assessing product availability and you may also find that mortgage sourcing systems cannot differentiate the issuer of a CCJ or Default, for example, communications or utilities.

That’s why at 3mc we have produced a secret adverse reference table to assist when looking to source your specialist enquiries. The table highlights the CCJ’s, Default’s and missed unsecured payments a lender will accept before assessing the lender plan options. As an example, Bluestone Mortgages ignore all CCJ’s and Defaults below £300, no matter the number or when registered as well as ignoring any amount telecoms CCJ’s and defaults. In this scenario your client would qualify for their cheapest plan option, known as the Clear Range.

You may find that if you used a sourcing system only to source this type of enquiry that the results which are returned may well be for a more expensive product plan than the plan your client would actually qualify for… In effect quoting inaccurately, which could then result in the client not commencing their mortgage journey with you as their adviser.

Let me illustrate this further with 2 different first-time buyer examples whereby we have used 2 different mortgage systems and applied our own research. Let me caveat this… the rates detailed are the cheapest initial rate and are not based on a total to pay assessment. The products and criteria illustrated are correct as at 11/01/2023.

In the above example, Precise Mortgage products have been removed as they will not allow any defaults registered in the 3 months before application.

In summary, understand your clients credit file, especially the issuer of the adverse credit, as this can impact on your lender and product selection.

Do not rely on just a basic mortgage source, there are other tools available, including mortgage packagers, such as 3mc.

📱 0161 962 7800

📧 info@3-mc.com

🌐 www.3-mc.com

*3mc for intermediaries only*

Please feel free to sign up to our Free Weekly Newsletter.